I delayed getting this email out a few days, because I wanted to be able to share that we have officially closed escrow on the first two deals from our fund, and we are very pleased with the outcome. More on that below.

California lawmakers passed one of the biggest rollbacks of the California Environmental Quality Act (CEQA) in state history, a move widely seen as a game-changer for urban housing development.

Tucked into the state’s budget housing bill and quickly signed by Governor Newsom, the new law exempts most infill housing projects (on parcels under 20 acres) from CEQA review. That means no more mandatory studies on traffic, air quality, noise, groundwater, or historical impacts for qualifying urban projects. In short: less red tape, fewer lawsuits, and faster timelines. CEQA is arguably one of the most abused laws in the State and a primary cause of the housing affordability crisis.

This is a huge victory for the pro-housing crowd (YIMBYs) and a potential unlock for California’s ambitious goal of building 2.5 million homes by 2030. Transit-oriented and student housing, often targets of CEQA litigation, will now move forward without being tied up in court for years.

Assemblymember Buffy Wicks, who introduced the overhaul, put it bluntly: “Saying ‘no’ to housing in my community will no longer be state-sanctioned.” And she’s right—this change removes one of the most notorious bottlenecks in the housing approval process.

CEQA was never about banning development; it was about disclosing environmental impact. But over the years, it became a weapon to block housing. This reform shifts the state toward “yes in my backyard” in a very real way.

Is this the silver bullet for affordability? No. But for those of us trying to build housing in California, this is the most meaningful structural change in decades.

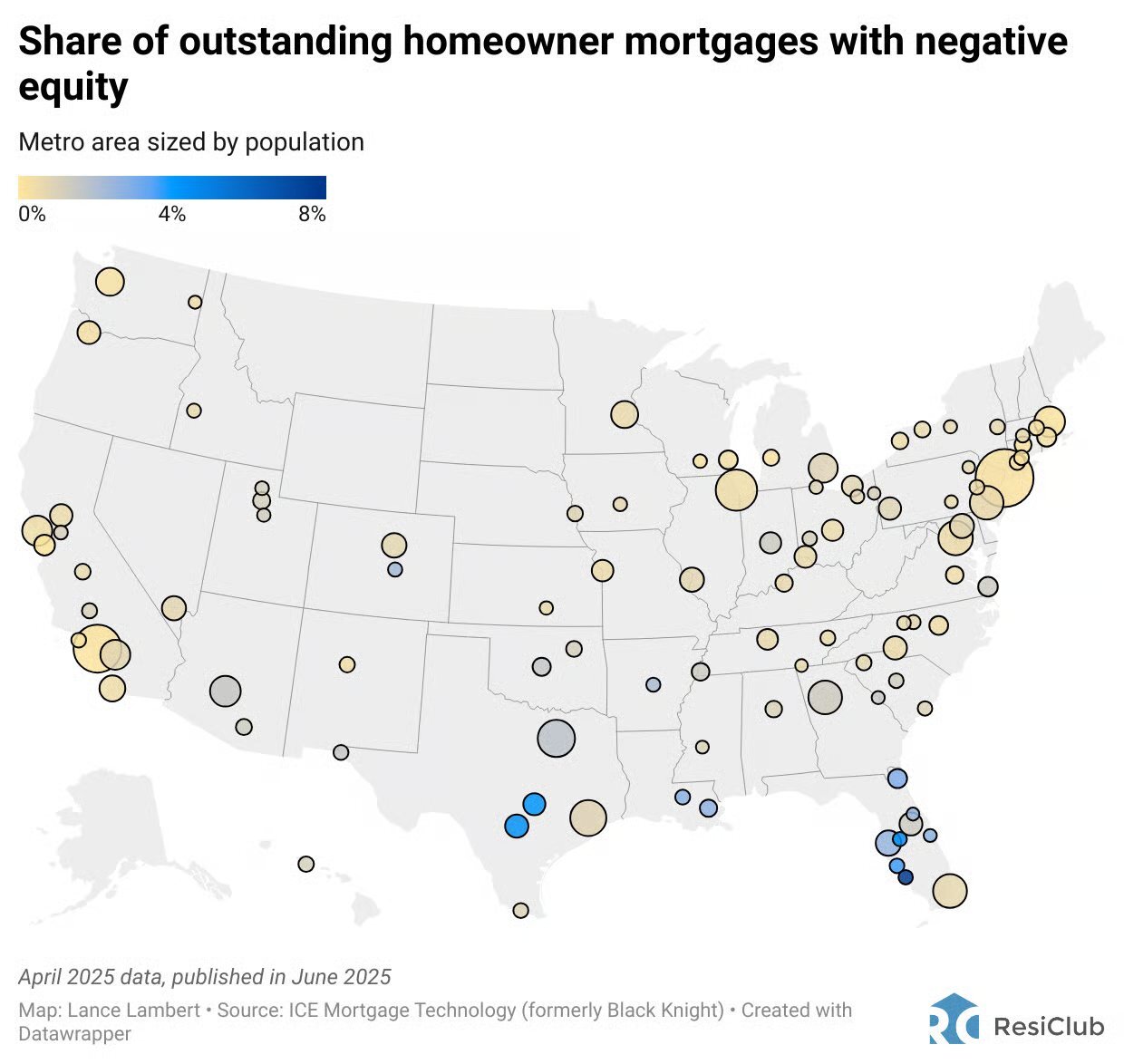

The last thing I want to share before getting into our regular content is this map; it is devastating for Texas and Florida. Keep this map showing the percentage of homes with negative equity per market in mind whenever you read statistics about the national housing market. Negative equity is a very bad indicator for a housing market.

Coastal California negative equity is essentially non-existent; Texas and Florida, not so much.

Real estate is a hyperlocal business.