Marterra Market Monitor - December 2024

Trump is a real estate guy, so he will be good for real estate, right?

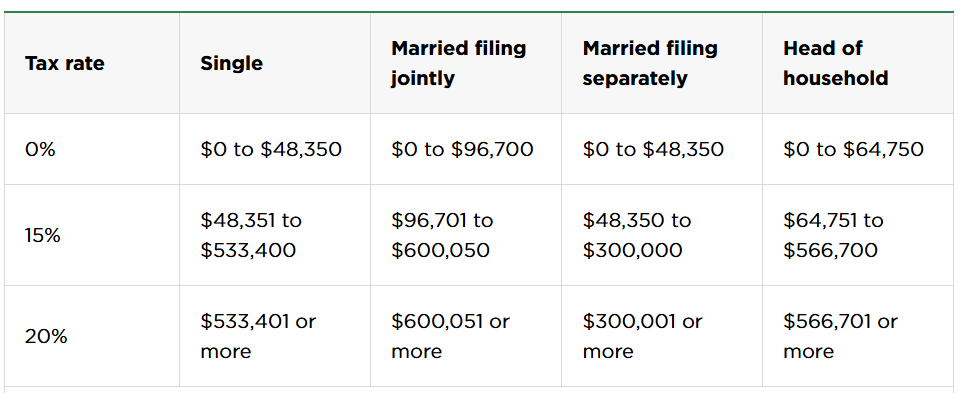

Have you heard of capital gains tax before?

So, question… if the city isn’t really reviewing these applications, and no one is inspecting them, what are we paying for? Aren’t permits supposed to be on a “fee for service” basis?

Christine Morgan | July 15, 2026

Daniel Morgan | July 1, 2026

June 15, 2026

Daniel Morgan | June 1, 2026

May 16, 2026

Where coastal OC buyers are finding value this spring -- Huntington Beach, Costa Mesa, Seal Beach, and the inland new-construction play in south OC.

May 1, 2026

Median prices, inventory, mortgage rates, and what spring 2026 means for OC buyers and sellers

Daniel Morgan | May 1, 2026

Daniel Morgan | April 1, 2026

Daniel Morgan | March 2, 2026

February 2, 2026

I haven't been able to get anyone to pay attention.

January 1, 2026

If you are reading this, congrats you made it to 2026.

April 21, 2025

Here are a few tips to help you stay ahead of water.

Daniel Morgan | April 22, 2025

Here’s how to sell quickly and maximize your return.

Daniel Morgan | May 6, 2025

wanted to kick off with a summary of a new California state assembly bill

Daniel Morgan | June 3, 2025

I’d like to invite you to schedule a one-on-one conversation about where you are at.

Daniel Morgan | July 3, 2025

California lawmakers passed one of the biggest rollbacks of the California Environmental Quality Act

Daniel Morgan | August 4, 2025

Summer is almost over and the kids are heading back to school.

September 9, 2025

I want to share a story so absurd it might help explain why I would do something so obviously against my own self-interest.

Daniel Morgan | October 2, 2025

We were hiring a new Director of Operations.

Daniel Morgan | November 2, 2023

Daniel Morgan | October 1, 2023

Daniel Morgan | July 1, 2023

Monthly Market Insights

Daniel Morgan | September 1, 2023

Daniel Morgan | March 3, 2023

Monthly Market Insights

Daniel Morgan | October 1, 2023

Daniel Morgan | September 10, 2024

Daniel Morgan | November 4, 2024

Daniel Morgan | December 6, 2024

investment property

March 1, 2023

Daniel Morgan | May 1, 2023

Monthly Market Insights

Daniel Morgan | April 1, 2023

Monthly Market Insights

Daniel Morgan | February 1, 2023

Monthly Market Insights

Daniel Morgan | April 18, 2025

Daniel Morgan | April 15, 2025

Daniel Morgan | April 7, 2025

April 4, 2025

Daniel Morgan | April 4, 2025

Daniel Morgan | March 25, 2025

Daniel Morgan | March 21, 2025

Daniel Morgan | January 8, 2025

Daniel Morgan | January 2, 2025

Daniel Morgan | December 16, 2024

Daniel Morgan | December 9, 2024

Daniel Morgan | October 2, 2024

investment property

Christine Morgan | February 18, 2024

Riley Spear | February 21, 2023

At Marterra Real Estate, we know that real estate gives you the power to define your life on your terms, and we’re honored to be a part of whatever’s next. Here, you have access to more than just knowledgeable, skilled agents. You have a team of trusted advisors at your side, working with a calm, relaxed demeanor as they guide you on your journey toward building wealth through real estate

Marterra Real Estate | CA DRE# 02014153

154 BROADWAY COSTA MESA CA 92627