Marterra Market Monitor - October 2024

Year To Date Activity

Properties Sold (single and multifamily): 35

Sales Volume: $45,977,087

Properties Leased: 75

Gross Collected Rent: $6,862,377

Brokerage Listings

Property Management Rental Listings

I have made a concerted effort over this election season to avoid politics as much as possible, and I am going to continue to avoid politics up until it is directly related to topics of concern related to the subject matter of this newsletter. So with that said, I wanted to briefly discuss Prop 33. Prop 33 seeks to repeal Costa-Hawkins Rental Housing Act of 1995, which currently prohibits local ordinances limiting initial residential rental rates for new tenants or rent increases for existing tenants in new construction and single family residential properties.

Here is a link to a non-partisan description of the proposition from the Secretary of State.

I would like to ask you to consider voting 'no' on Prop 33. Rent control doesn't work the way it is intended to and often leads to worse outcomes for the very people it is intended to help. Here is a link to a California YIMBY article that summarizes in plain English a very dense article from the Journal of Housing Economics that synthesizes the finding of 112 empirical studies on the impacts of rent control. The TLDR: rent control is bad for everyone, everyone except NIMBYs.

If you want to chat about rent control or Prop 33, please reach out.

A last bit of housekeeping. We have two events coming up that I would like to invite you to:

1. Commercial Real Estate Happy Hour - we are co-sponsoring an event October 16th at the Wild Goose from 5:30-7:30pm. Registration is both required and free - register here.

2. A conversation with John Stephens (Costa Mesa Mayor) Jeff Harlen (Costa Mesa Mayor Pro Tem) October 17th at our office from 5:30-7pm. Light refreshments will be provided. Space is limited - so please make sure you RSVP to me via email at [email protected].

Now back to our regularly scheduled programming.

Single-Family Transactional Market: As the old saying goes, pigs get fat, and hogs get slaughtered, especially as we move into the slower holiday season.

We have witnessed sellers, especially of vacant properties, hold out for a higher price only to accept a lower price months later. Sellers should evaluate pricing and timing, especially if they have higher carrying costs.

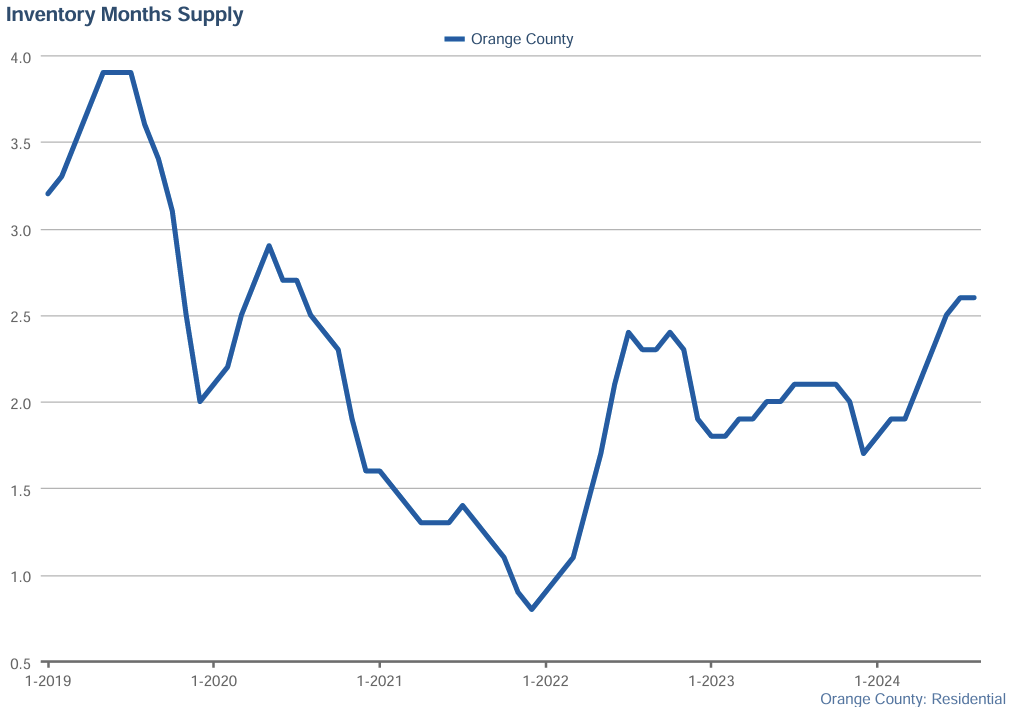

Orange County has a housing supply of 2.6 months, the highest reading since July/August 2020. Generally, a market with 6 months supply is considered to be balanced. The inventory levels are still considered tight, but they have definitely trended up, and I expect that trend to increase through the end of the year.

Residential Leasing Market: As we head into fall, the leasing season is wrapping up. We only have a few properties available for lease. At this time of the year, I highly recommend property owners to drop rents to fill their properties. Once Halloween hits, very few people move until at least the new year. Giving up a few hundred dollars of rent is preferable to having a few months of vacancy.

I will make this section optional from now to the end of the year.

Mortgage Rates/Market: This month, I wanted to take some time to go over mortgage points. Paying points on a mortgage (also known as "buying down the rate") can make sense in certain situations where the long-term benefits of a lower interest rate outweigh the upfront cost.

Here’s A Breakdown Of When It May Be A Good Idea:

Staying in the Home for a Long Time: If you plan to stay in the home for an extended period, paying points can save you money in the long run by reducing your monthly payments and the total interest you pay over the life of the loan. For example, if you plan to stay in the home for 10 or more years, paying points could make sense because you'll benefit from the lower interest rate over time.

Break-Even Point Analysis

Break-Even Point is Favorable: The break-even point is when the amount you saved in interest payments equals the amount you paid for the points. If the break-even point occurs early in your homeownership (within a few years), it may be worthwhile to pay points.

You can calculate this by dividing the cost of the points by the monthly savings to see how long it takes to recover the upfront cost.

Lower Monthly Payments

Need for Lower Monthly Payments: If your goal is to have lower monthly payments for budgeting reasons, paying points upfront can help you achieve that by lowering the interest rate and, subsequently, your monthly mortgage payment.

This can be useful if you are optimizing for cash flow.

High Interest Rate Environment

Current Interest Rates are High: If mortgage rates are high at the time you're locking in your loan, paying points to lower your rate can be a smart move if you think rates won't drop significantly in the near future.

Tax Deductibility

Potential Tax Deduction: Mortgage points are often tax-deductible in the year they are paid if the loan is for a primary residence (check with a tax professional for your specific situation). This can lessen the effective cost of paying points.

When It May Not Make Sense:

Short-Term Ownership: If you plan to sell or refinance the home within a few years, paying points may not be cost-effective, since you won’t stay in the home long enough to realize the long-term savings.

Other Financial Priorities: If you need your savings for other investments, emergency funds, or debt payments, it might be better to avoid paying points and keep that money liquid.

Grant Sedlak

VP of Mortgage Lending

310-924-0777

[email protected]

Commercial Real Estate (CRE): I went to a real estate conference last week, and everyone seemed pretty optimistic. Well, everyone except for the folks who invest in office...they're still pretty depressed. Things are very tough for most of the commercial real estate world, so I suspect much of the optimism was really just a coping mechanism.

It's not just office. Anyone who backed up the truck on cheap floating-rate debt is getting rekt (the Gen Z spelling of wrecked).

In past editions of the market monitor, I have picked on multifamily syndicators (namely Tides Equities). However, hotel investors have been reckless as well. Look at this 5-year stock chart for Ashford Hospitality Trust.

From $342 to $0.75 per share.

If you have been to Walgreens (or Rite Aid or CVS, for that matter), you probably will not be surprised to hear that Walgreens is closing 25% of its stores or almost 2,150 stores.

If you are surprised, it's probably because they are only closing 25% of their stores.

The funny/sad thing is that investors nationwide bought single-tenant triple-net retail investments because the properties were leased by "credit tenants." A credit tenant is a tenant with exceptionally good credit, such that the lender to the landlord has very high assurance of timely payment of principal and interest.

The funnier/sadder thing is that Walgreens proved to be a "credit tenant" rather than an actual credit tenant.

The good news for the property owners who leased to Walgreens is that Walgreens is obligated to pay their rent through the remainder of their lease. The average remaining lease term for Walgreens is 9.3 years. Think about how bad your business has to be for it to make sense to pay rent and not open your doors for business.

The bad news is that the most common replacement use is discount stores (think the 99-cent store or Dollar General), which generally pay about half the rent that a Walgreens would pay.

It feels appropriate to share the old real estate adage

Don't buy the tenant, buy the real estate

I want to shout out to Daniel Herrold at Northmarq - a lot of the Walgreens detail came from Daniel's newsletter. Daniel is organizing the happy hour mentioned above.

If you are interested in signing up for his newsletter, you can do so here.

Macro Observations: Folks, we have nothing to worry about.

"Overall, the economy is in solid shape; we intend to use our tools to keep it there."

- Jerome Powell, 9/30/2024.

There are some indications that the economy is doing great.

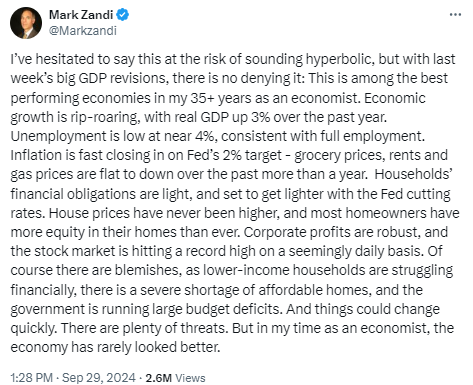

According to Mark Zandi, Moody's Chief Economist, it is one of the best economies he has ever seen.

Mark is correct: GDP is strong, unemployment (nationally) is low, and inflation has continued to cool. But for the most part, these are all backward-looking metrics, not forward-looking indicators.

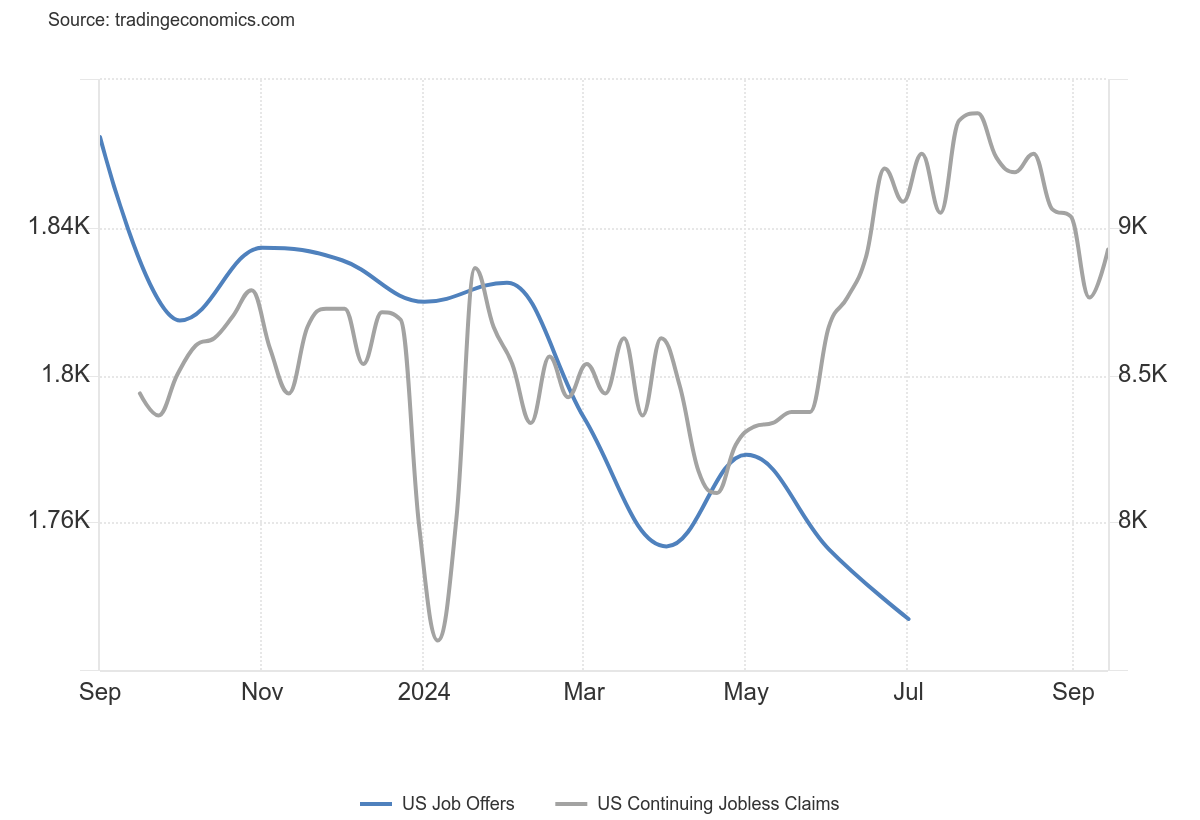

Some forward-looking indicators are giving us less confidence, namely the job market. The divergence between job openings and jobless claims is jarring.

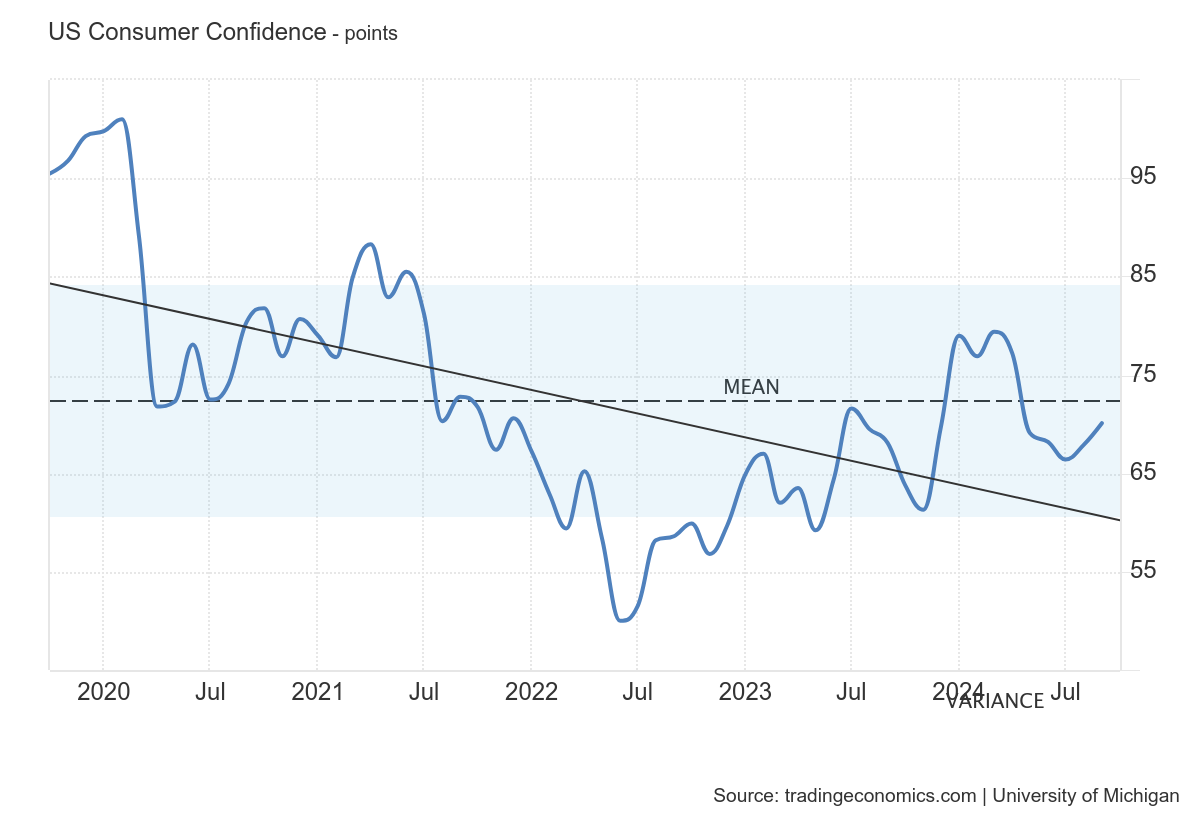

Below is the 5-year chart for the University of Michigan Consumer Confidence Index. More interesting to me than the downward trendline is that, while currently trending up, the reading is below the 5-year average. Even more surprising is that it is below the readings during the initial COVID shutdowns before PPP and stimulus had a chance to kick in.

I have struggled to understand how consumer spending has remained high in the face of a deteriorating job market and waning consumer confidence. But wealthy Americans (those who own assets) have fared much better over the last few years.

If asset prices fall, it should impact consumer spending habits for the wealthy and could have a material impact on the nation's GDP. It will be interesting to see what happens through the election and holiday season.

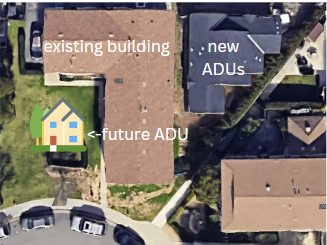

What's the Good Word: While California does a lot of really dumb things that discourage new construction (which in turn negatively impacts housing affordability), every now and then, they do something good. One of my favorite examples is the law allowing investors to build additional units on multifamily properties without going through a zone change. We have built a handful of units in Costa Mesa this way, like the units pictured below that we are building now.

As an investor and someone who cares about housing affordability, I love this strategy. We can generally earn about a 10% return on cost (which I believe is very good) on our new ADUs in Costa Mesa, and the units typically rent out for significantly less than new market-rate units. I recently compared units we built and leased out, and our rents were nearly 30% cheaper than new construction delivered in a reasonably comparable location. That is a win for the developer and a win for the community.

The state of California just passed SB 1211, which allows for the lessor of 8 additional ADUs or the number of existing units. Most cities will take at least one year to incorporate SB 1211 into their building codes. SB 1211 will create a lot of exciting opportunities.

Project Updates: We have several active projects; here is a quick update on two. We are always looking for more projects, so if you know of any, please reach out. If you have a property that you believe might be a good candidate for a project, we are happy to discuss partnering up on the project.

Mission Ave, Costa Mesa: We passed all of our utility inspections and have called for our fire sprinkler inspection (it's today!).; assuming we pass the inspection, we will have a clear path to receiving our certificate of occupancy which we need before we can lease out the units.

This property will be a good candidate for SB1211, and we should be able to add 1-2 more units in the front courtyard, which would bring the total unit count to 7-8 units (it was originally a fourplex).

36th Street, Newport Beach: We just got this property under contract for ~$2,400,000. It is currently configured as a duplex; we plan to convert it into a single-family home and permit and build an above-ground garage storage room into an ADU. This is going to be a fun one.

Thanks again for reading, and I would like to thank our agents and property managers who provide valuable insights from their day-to-day in the field. Without them, this email wouldn't be very useful or interesting.

If there is anything you need: vendors, lenders, or others, please let me know. We have an extensive network of the best and brightest in the industry.

I geek off this stuff; if you want to grab a coffee or chat about anything related to real estate, the market, or investing, please do not hesitate to reach out.

If you don't want to receive these updates in the future, please smash the unsubscribe button below. No hard feelings; I do it ruthlessly. Lastly, if you found the above informative, please share it with a friend or drop me a line.

Daniel Morgan

Managing Principal

949-413-0912

[email protected]

Lic# 01901285

Christine Morgan | July 15, 2026

Daniel Morgan | July 1, 2026

June 15, 2026

Daniel Morgan | June 1, 2026

May 16, 2026

Where coastal OC buyers are finding value this spring -- Huntington Beach, Costa Mesa, Seal Beach, and the inland new-construction play in south OC.

May 1, 2026

Median prices, inventory, mortgage rates, and what spring 2026 means for OC buyers and sellers

Daniel Morgan | May 1, 2026

Daniel Morgan | April 1, 2026

Daniel Morgan | March 2, 2026

February 2, 2026

I haven't been able to get anyone to pay attention.

January 1, 2026

If you are reading this, congrats you made it to 2026.

April 21, 2025

Here are a few tips to help you stay ahead of water.

Daniel Morgan | April 22, 2025

Here’s how to sell quickly and maximize your return.

Daniel Morgan | May 6, 2025

wanted to kick off with a summary of a new California state assembly bill

Daniel Morgan | June 3, 2025

I’d like to invite you to schedule a one-on-one conversation about where you are at.

Daniel Morgan | July 3, 2025

California lawmakers passed one of the biggest rollbacks of the California Environmental Quality Act

Daniel Morgan | August 4, 2025

Summer is almost over and the kids are heading back to school.

September 9, 2025

I want to share a story so absurd it might help explain why I would do something so obviously against my own self-interest.

Daniel Morgan | October 2, 2025

We were hiring a new Director of Operations.

Daniel Morgan | November 2, 2023

Daniel Morgan | October 1, 2023

Daniel Morgan | July 1, 2023

Monthly Market Insights

Daniel Morgan | September 1, 2023

Daniel Morgan | March 3, 2023

Monthly Market Insights

Daniel Morgan | October 1, 2023

Daniel Morgan | September 10, 2024

Daniel Morgan | November 4, 2024

Daniel Morgan | December 6, 2024

investment property

March 1, 2023

Daniel Morgan | May 1, 2023

Monthly Market Insights

Daniel Morgan | April 1, 2023

Monthly Market Insights

Daniel Morgan | February 1, 2023

Monthly Market Insights

Daniel Morgan | April 18, 2025

Daniel Morgan | April 15, 2025

Daniel Morgan | April 7, 2025

April 4, 2025

Daniel Morgan | April 4, 2025

Daniel Morgan | March 25, 2025

Daniel Morgan | March 21, 2025

Daniel Morgan | January 8, 2025

Daniel Morgan | January 2, 2025

Daniel Morgan | December 16, 2024

Daniel Morgan | December 9, 2024

Daniel Morgan | October 2, 2024

investment property

Christine Morgan | February 18, 2024

Riley Spear | February 21, 2023

At Marterra Real Estate, we know that real estate gives you the power to define your life on your terms, and we’re honored to be a part of whatever’s next. Here, you have access to more than just knowledgeable, skilled agents. You have a team of trusted advisors at your side, working with a calm, relaxed demeanor as they guide you on your journey toward building wealth through real estate

Marterra Real Estate | CA DRE# 02014153

154 BROADWAY COSTA MESA CA 92627