Year To Date Activity

Properties Sold (single and multifamily): 30

Sales Volume ($): $40,592,587

Properties Leased: 59

Gross Collected Rent: $6,073,696

What part of the cycle are we in?

The part when NVIDIA, the darling AI stock, earnings release exceeds expectations, and then the stock proceeds to lose 10% overnight.

I had a conversation with Grant Sedlak (my friend who provides the mortgage insights for this newsletter) last week, and he casually mentioned that many cash purchases in affluent areas are being refinanced shortly after closing or are funded with securities-based lines of credit, loans against stocks and bonds not held in retirement accounts.

Much like other asset-backed securities, the loan amount is based on a percentage of the value of the assets, in this case, the securities. An interesting thing about securities is that we know what their value is in real-time, so it is very easy for the lender to determine if the loan to value changes. Sometimes, when the value decreases, and the loan to value increases over the threshold that the lender wants, the lender will request the borrower send over funds to bring the loan to value back in line with the approved thresholds, this is called a margin call.

As you will see later on in this market monitor, rate cuts are happening, and they are happening this month! So stocks should go to the moon, right?

Not so fast, as we will discuss later; rates are getting cut because we are seeing accelerating weakness in the labor market, which should ripple through the economy via weaker consumer spending.

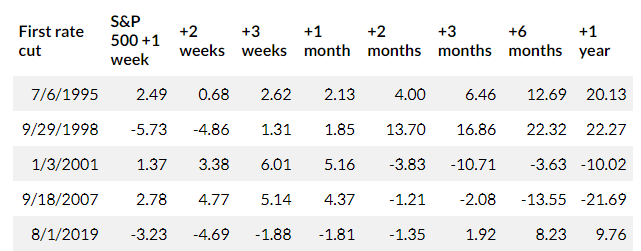

How have we faired in the past? Not so great. Out of the last five rate cut cycles, only once ('95) has the stock market not experienced losses within a year of the first rate cut.

So, what will the ripple effect be of a declining stock market? A reversal of the wealth effect. The wealth effect is a behavioral economic theory that states that people spend more when the value of their assets increases. In addition to a moderation or decrease in the amount of money available from asset-backed securities, we expect to see a broader decrease in consumer confidence and spending.

Don't worry; the kids are back in school, the Fed is set to lower interest rates, and all is right with the world.

For the first time in a while, it feels like an investment opportunity is on the horizon, and we are gearing up to capitalize on these opportunities.

We're all going to make it, fam.

Single-Family Transactional Market: During last week's weekly call with our brokerage team, I asked all of our agents about their sense of "buyer demand". The consensus was:

We have buyers, and there are buyers looking at our listings, but all the buyers have very little sense of urgency unless the home (or price) is perfect.

From conversations with friends and clients, I have noticed a lot of pent-up demand (and supply) from move-up buyers. Many people purchased homes before the pandemic, and their cost of ownership is very low due to a low property tax basis and sub-3 % interest rates. Many of these people will stay in their homes for an extended time, but others will start to move, especially as the gap between their interest rate and current rates starts to narrow.

Lastly, this is not an observation from the transactional market, just the view from one of our current listings.

Residential Leasing Market: We had a lot of units for rent over the last month (not because of turnover, but because we onboarded a bunch of property management clients), and the leasing market was noticeably slower than in previous months. During August, we had 12 units on the market and we leased out 6. Nearly every unit we leased out had its asking price reduced.

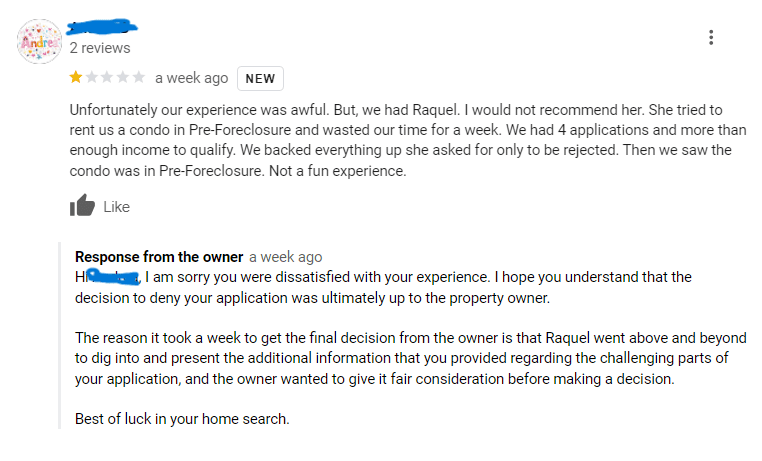

Another observation from our leasing process. There is a measure of the economy known as the misery index. It is calculated by adding the unemployment rate and the rate of inflation. Without formally calculating the misery index, it has been pretty apparent to us that the misery index is VERY high right now, and people are generally pissed off at life; this is especially true for prospective tenants as moving is stressful, inventory is tight, and rents are high. We deal with thousands of prospective tenants per year (we had over 5,000 inquiries in '23), and generally, most are polite and professional, with a few exceptions. Lately, there has been a notable increase in "exceptions".

Exhibit A: The lady below gave us a one-star review on Google because her application was denied, and it took a week to formally reject it.

Her application was rejected because her credit score was in the mid-400s. It took us a week to respond because she sent us additional documentation to justify the credit score, and our colleague Raquel spent a lot of time verifying the information they provided but was not able to do so.

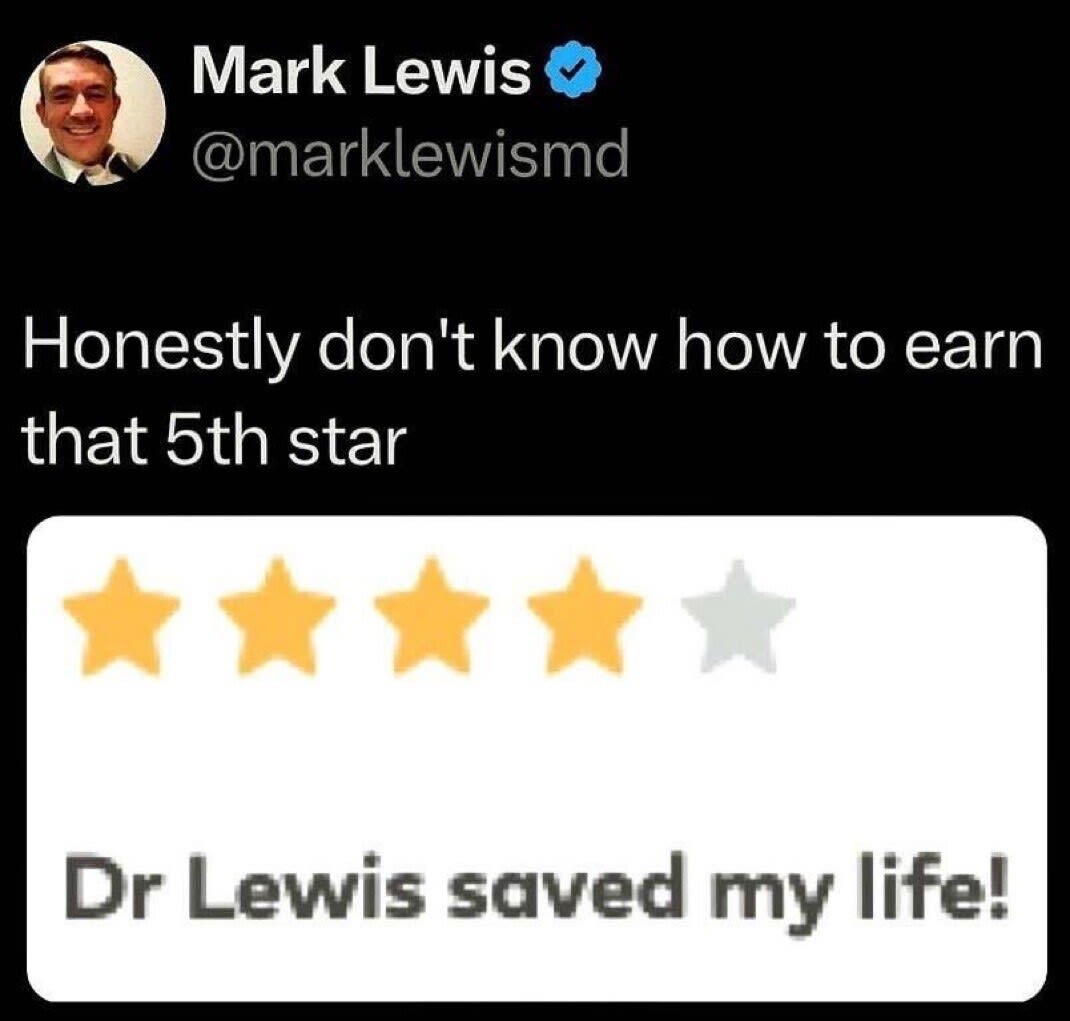

It's not just us getting less-than-ideal reviews.

Online reviews are very important to our business, and bad reviews like this can hurt it. So, if you have had a good experience with our team, please consider leaving a review on Google and Yelp.

Mortgage Rates/Market: Major news emerged from the Federal Reserve's retreat in Jackson Hole on Friday, as Jerome Powell called for a policy shift, indicating a potential rate cut in September. This anticipated move is likely to be priced in by many lenders ahead of time. When the Fed discusses adjusting rates, they are referring to the Fed Funds rate, which directly impacts HELOCs, auto loans, credit cards, and savings accounts. People with adjustable-rate HELOCs or those applying for auto loans will benefit from this rate cut, though they may also see a decrease in the interest paid on their savings accounts, which is a downside. Currently, FHA rates are in the mid-5% range, conforming rates are in the high 5% to low 6% range, while Jumbo and Non-QM programs are in the low 6% range.

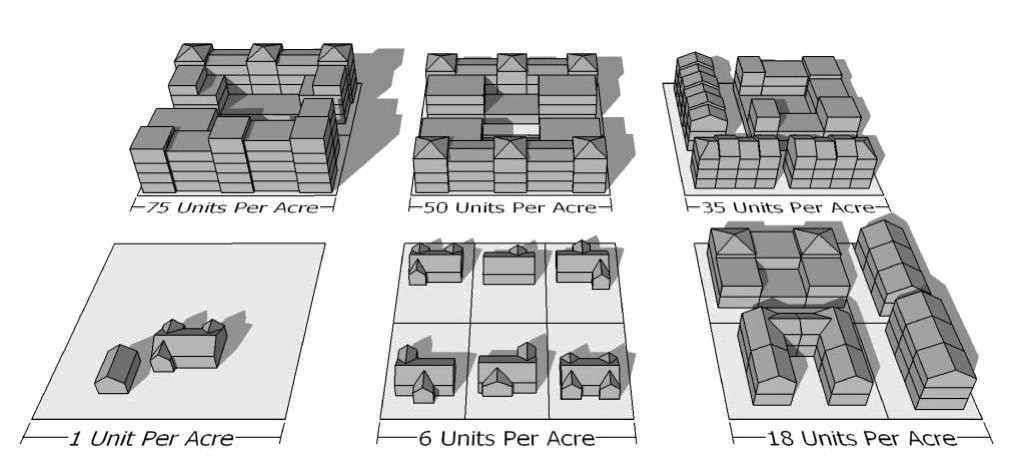

Commercial Real Estate (CRE): The Ziggurat building, the unofficial official location where nearly every teenager in Southern Orange County learned to drive for the last +40 years, is up for auction.

The property, which is owned by the General Services Administration (the Federal Government), covers approximately 91 acres. A study conducted by the Urban Land Institute suggested that the City of Laguna Niguel should allow between 2 and 4K residential units on the property, at roughly 60-80 units per acre.

For those of you unfamiliar with what various density looks like, see below.

Three bidders have submitted 72 bids and have pushed the price to a whopping $152M.

While this price feels astronomic, the real question is:

What will impact car insurance rates when teenagers are forced to learn to drive on actual streets?

Macro Observations: Non-farm payrolls were revised down by 818k for March 23-24. This is in addition to the downward revisions we have received every month. In total, the revisions are approximately five times what we usually see. All of this is to say that the state of our employment market and our overall economy is nowhere near as strong as the data previously suggested.

Jerome Powell has seen enough.

“The time has come for policy to adjust. The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

You can mark your calendar for September 18th. Powell was pretty direct in telling us that we are entering a rate-cutting cycle.

With the 18th being about three weeks out, we have ample opportunity for the incoming data to impact the Fed's decision on pace/forward guidance.

As excited as I am that rate cuts are finally upon us, I think it is important to reiterate the reason that rates are getting cut is that the economy sucks, and the rate at which it's sucking is accelerating. The Fed must balance keeping inflation at bay (not cutting rates too fast) and preventing the economy from crashing (cutting rates too slowly) to achieve what economists call a soft landing. If it sounds like a challenging task, that is because it is, and it's generally accepted that the Fed has only pulled it off once in 60 years.

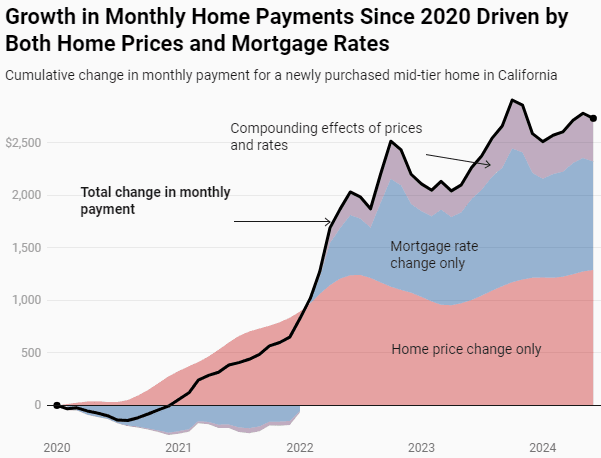

What's the Good Word: Home affordability is atrocious, especially in California. The drivers behind the affordability issues are obvious: interest rate increases and increased home prices.

Fortunately, with rate cuts on the horizon, prospective homebuyers will see some relief as mortgage rates decline. Unfortunately, given how incredibly challenging it is to build in California, supply will likely remain extremely tight for the foreseeable future.

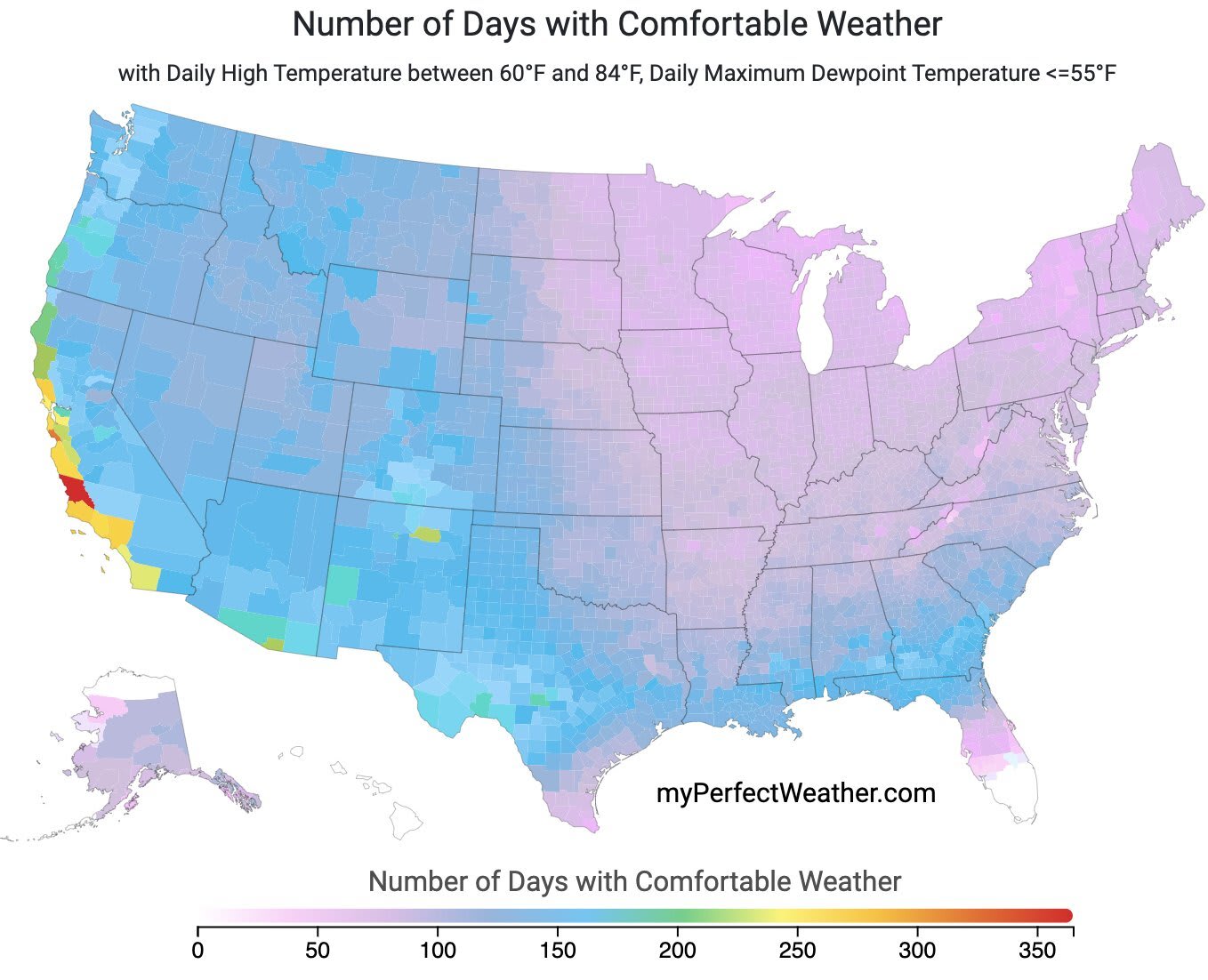

High earners will continue to want to live in the nicest locations in the US, and as you can see below, Coastal California has demonstrably better weather than the rest of the county.

Given the supply constraints and structural support demand, home price reductions will likely provide little relief.

Conor Sen, founder of Peachtree Creek Investments, penned an a piece for Bloomberg titled "Homes Will Be Affordable Again—Just Not Anytime Soon" that is worth a read the TLDR is that "restoring purchasing power entails a slow grind of rising wages, falling mortgage rates, and modest home-price gains".

I would also add, especially for California, the construction of new homes and lots of new homes, but that probably won't happen, at least not at the scale required.

Project Updates: We have several active projects; here is a quick update on two.

Hopefully, I can share more in the month or so, but we are gearing up to get very active in the investment space, please reach out if you know of a project that might be a good fit or have a project and would like a partner.

Mission Ave, Costa Mesa: We are wrapping up final inspections to allow for utility hookups. From there, we will call for the final inspection and push for a certificate of occupancy. Hopefully, we will be on the market in the next 30 days or so.

Undisclosed Location, Costa Mesa: We received the final sign-off on our electrical panel upgrade, completed a reroof, and finished re-piping the property. Last Tuesday (when these photos were taken), we started the build-back process. Once the build-back is complete, the fun part starts.

Thanks again for reading, and I would like to thank our agents and property managers who provide valuable insights from their day-to-day in the field. Without them, this email wouldn't be very useful or interesting.

If there is anything you need: vendors, lenders, or others, please let me know. We have an extensive network of the best and brightest in the industry.

I geek off this stuff; if you want to grab a coffee or chat about anything related to real estate, the market, or investing, please do not hesitate to reach out.

If you don't want to receive these updates in the future, please smash the unsubscribe button below. No hard feelings; I do it ruthlessly. Lastly, if you found the above informative, please share it with a friend or drop me a line.